Commentary

The youthful generations ought to ignore the chart beneath that’s typically seen in quite a lot of varieties in the monetary media touting “how straightforward it’s to develop into a millionaire.” There are two main causes millennials aren’t saving as they need to. The first is the lack of cash to save lots of, and the second is that markets don’t compound returns.

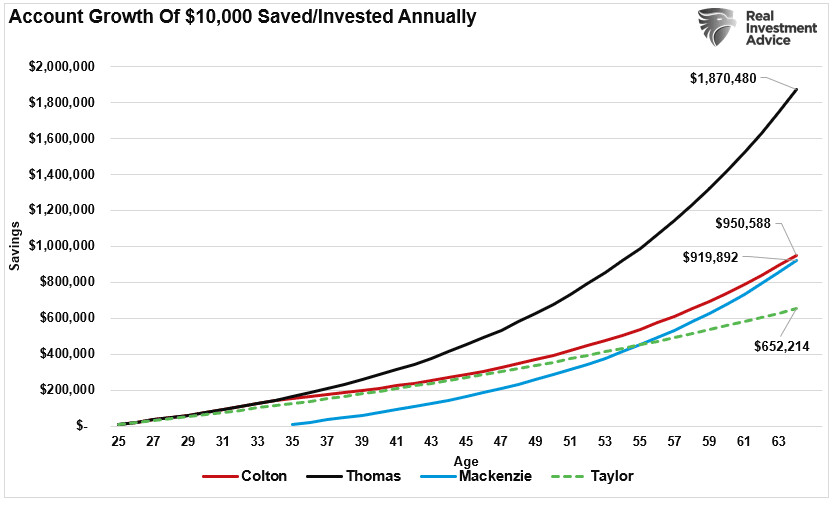

The following chart depicts 4 hypothetical millennial buyers who make investments $10,000 a 12 months at a 6.5 p.c annual price of return over totally different intervals of their lives:

- Thomas invests for his total working life, from 25 to 65.

- Mackenzie begins 10 years later, investing from 35 to 65.

- Colton places cash away for less than 10 years at the begin of his profession, from 25 to 35.

- Taylor saves from 25 to 65, like Thomas, however as an alternative of being reasonably aggressive along with her investments, she merely holds money at a 2.25 p.c annual return.

At first look, it’s obvious that beginning a constant saving and investing program early in life results in the greatest monetary outcomes. Of course, such is completely logical.

However, there are two essential issues with the evaluation that renders its observations irrelevant.

The Saving Problem

The first drawback is kind of evident when current monetary surveys of common Americans. For instance, a current Bankrate survey discovered:

“Only about 4 in 10 Americans have sufficient savings to cowl an unplanned expense of $1,000, which means greater than half would want to seek out different means to pay for an sudden automobile restore or emergency room go to.”

Of course, with inflation surging in 2022, one other more moderen Bankrate examine discovered that greater than half of adults are uncomfortable with their degree of emergency financial savings.

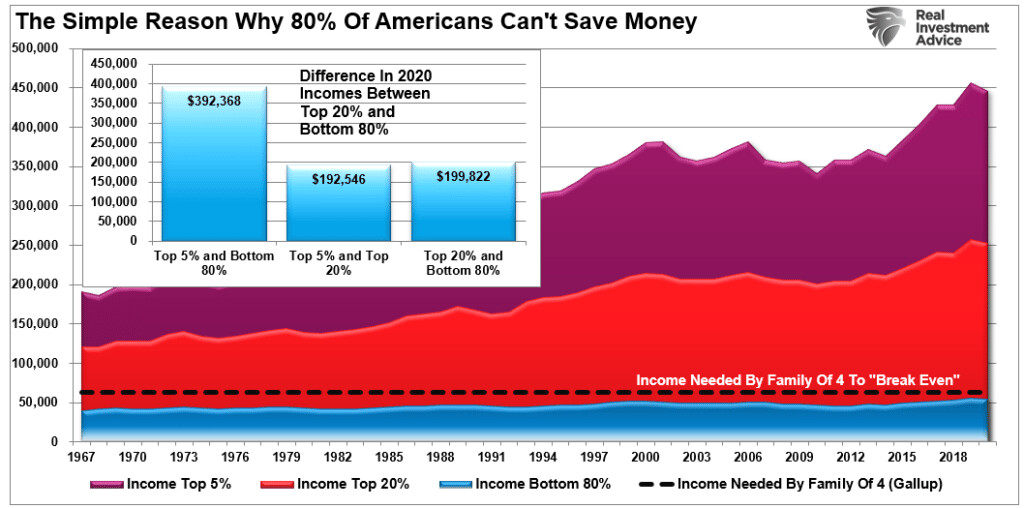

For most millennials, the concept of saving $10,000 a 12 months sounds nice; the drawback is that the median earnings in the United States barely covers the price of residing, a lot much less leaving extra financial savings. As proven, the median earnings in the United States for 80 p.c of wage earners is $53,663 (through the Census Bureau, 2020 most up-to-date knowledge).

The drawback is, in fact, the generalized assumption that millennials are in a position to save roughly 25 p.c of their annual aftertax incomes. This is just not a practical assumption, provided that lots of the millennial age group are fighting pupil mortgage and bank card money owed, automobile notes, condo lease, and many others.

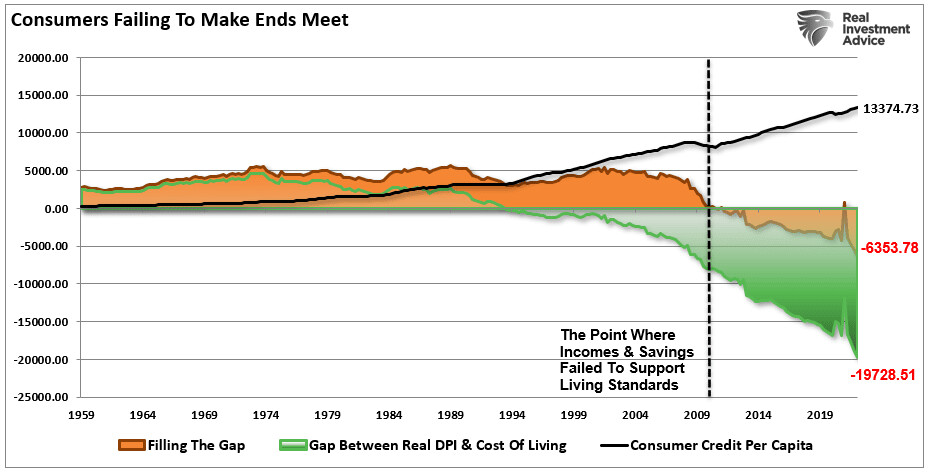

In truth, the present hole between financial savings/earnings and the price of residing is operating at the highest annual deficit on document. It presently requires roughly $6,300 a 12 months in further debt to take care of the present lifestyle. Either that or spending will get decreased, which is the doubtless final result as a recession turns into extra seen.

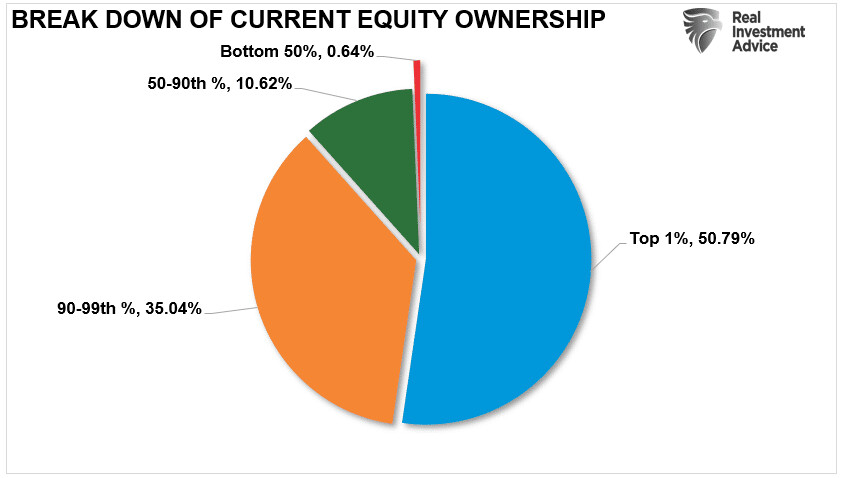

Of course, in case you don’t have extra money movement, it’s actually tough to put money into the monetary markets. That’s why these in the prime 10 p.c of earnings earnings personal roughly 90 p.c of the total inventory market.

Therefore, when it’s understood about the lack of monetary stability in the overwhelming majority of households, how are Thomas, Mackenzie, Colton, and Taylor supposed to save lots of $10,000 a 12 months? That’s a questionable proposition when Thomas works in customer support, Mackenzie is a nursing assistant, Taylor is a bartender, and Colton works retail. These are the jobs which have made up a bulk of the employment will increase since 2009. They are also in the decrease wage-paying scales, which makes the drawback of financial savings tough.

That’s why, in line with the Pew Research Center, millennials are setting new information for residing with their dad and mom.

“Young folks began shifting out midcentury as they grew to become extra economically impartial, and by 1960 solely 29 p.c of younger adults complete—women and men—have been residing with mother and pa. But that quantity has been rising ever since, and in 2021, the variety of younger adults residing with their dad and mom eclipsed the Nineteen Forties. And final 12 months, 52 p.c of younger adults have been residing at house, which is the highest price since 1940.”

Stocks Do Not Deliver Compound Rates of Return

The second main drawback with the evaluation is the assumption that shares ship compounded returns over the long run. This is certainly one of the largest fallacies perpetrated by Wall Street on people in the effort to entice them to sink their cash in fee-based funding methods and overlook about them.

Compound returns solely happen in investments which have a return of principal operate and an rate of interest, equivalent to CDs or bonds (not bond funds). This is just not the case with shares, as only in the near past mentioned in the “Problem with HODL” (maintain on for pricey life).

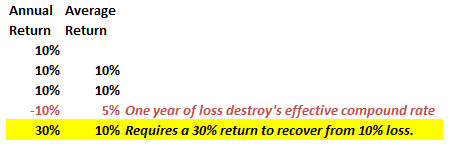

“While the common price of return might have been 10 p.c over the long run, the markets don’t ship 10 p.c yearly. Let’s assume an investor desires to compound their returns by 10 p.c a 12 months over 5 years. We can do some fundamental math”:

“After three years of 10 p.c returns, a drawdown of simply 10 p.c cuts the common annual compound development price by 50 p.c. Furthermore, it then requires a 30 p.c return to regain the common price of return required.”

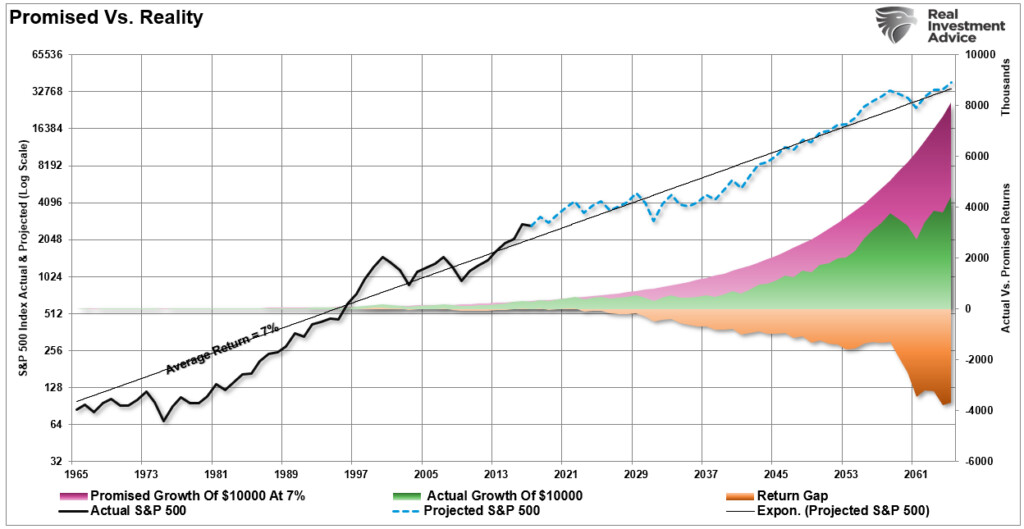

While an investor can “HODL” for the long run, there’s a vital distinction between the common and precise returns obtained. As I confirmed beforehand, the influence of losses destroys the annualized compounding impact of cash. The purple shaded space exhibits the common return of seven p.c yearly. However, the differential between the promised and precise return is the return hole.

When imputing volatility into returns, the differential between what buyers have been promised (and this can be a large flaw in monetary planning) and what really occurred to their cash is substantial over the long run.

Timing Is Everything

Last—and possibly the most crucial level—is the valuation degree of the market when these people started the saving and investing program.

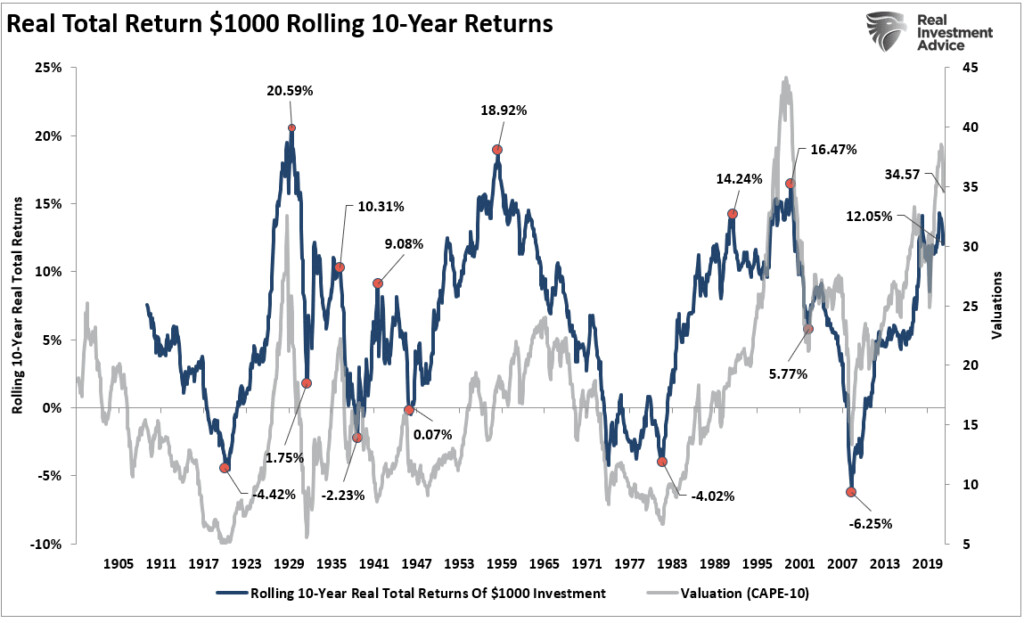

The drawback for Thomas and his mates is that valuation ranges are presently at a few of the highest ranges recorded in market historical past. The chart beneath exhibits actual rolling returns for stock-based investments over 20-year time frames at varied valuation ranges all through historical past.

The return has all the pieces with valuations and whether or not multiples are increasing or contracting. As proven in the chart above, actual charges of return rise when valuations broaden from low to excessive ranges. But actual charges of return fall sharply when valuations have traditionally exceeded 23 instances trailing earnings and revert to their long-term imply.

Yes, “purchase and maintain” investing will work, however that will depend on when you begin your investing journey. At 35 instances the cyclically adjusted price-to-earnings (CAPE) ratio, such means that returns over the subsequent 10–20 years might be disappointing.

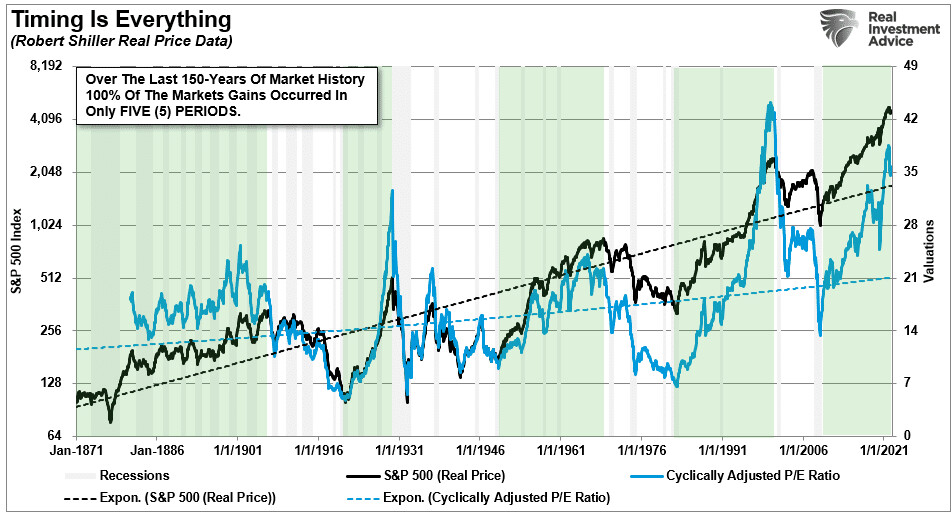

The majority of the returns from investing got here in simply 5 of the 9 main market cycles since 1871. Every different interval yielded a return that misplaced out to inflation throughout that time-frame.

Conclusion

While long-term and buy-and-hold funding methods sound good at face worth, the real-world outcomes fell brief for 3 causes:

- Lack of financial savings;

- Inability to stay constant; and

- Impact of unfavourable returns on long-term objectives.

Unfortunately, for people, the distinction between promised and precise outcomes continues to be two very various things, and customarily not for the higher.

It additionally ought to be considerably evident that long-term and buy-and-hold methods don’t work as promised when you think about the charts above. After three vital bull markets since 1980, the backside 80–90 p.c of Americans have little wealth to point out for it.

This is because of a myriad of poor funding selections, horrible recommendation from the monetary media, and a predatory Wall Street benefiting from unwitting buyers.

Don’t misunderstand me. Should people put money into the monetary markets? Absolutely. However, it ought to be completed with a stable funding self-discipline that takes into consideration the significance of managing volatility and psychological funding dangers. There are many nice advisers that do precisely that; sadly, they typically aren’t discovered on the entrance pages of funding publications or in the monetary media.

Of course, the drawback to resolve first is getting millennials out of their dad and mom’ basements and again into the workforce. Having a job makes it simpler to begin investing, to start with.

Views expressed on this article are the opinions of the writer and don’t essentially replicate the views of The Epoch Times.

Follow